UK Home Prices Surge £3,000 in April

The U.S. housing market is experiencing a nuanced shift, with average home prices seeing a modest increase, yet underlying factors suggest a more cautious environment for both buyers and sellers. In April, the typical asking price for a home rose by nearly $3,000 month-over-month, representing a 0.8% increase. While this marks a rise, it falls slightly below the historical average for April, which typically sees a 1.2% uptick. Across the nation, the average asking price in April stood at $373,971, an increase of $2,929 from the preceding month.

Several forces are shaping this market dynamic. Elevated mortgage rates, coupled with a significant number of sellers actively seeking buyers, are tempering the growth in new seller asking prices. Rightmove data indicates that the inventory of homes for sale is at an 11-year high for this time of year, creating a more competitive landscape for sellers.

Despite these headwinds, buyer demand has shown remarkable resilience, particularly among first-time homebuyers. This suggests that the current mortgage rate environment, while higher, is not deterring new entrants from exploring the market and making inquiries.

However, the recent price growth has been predominantly driven by higher-end properties, specifically those with four or more bedrooms. This segment of the market often includes cash purchasers who are less susceptible to fluctuations in borrowing costs.

Colleen Babcock, a property expert, commented on this trend. She noted, “With mortgage rates remaining elevated, it’s not surprising that price growth is proving strongest in parts of the market less exposed to higher borrowing costs, such as top-of-the-ladder homes, while sectors more exposed to interest rates are seeing slower momentum.”

Regional Strengths and Market Realities

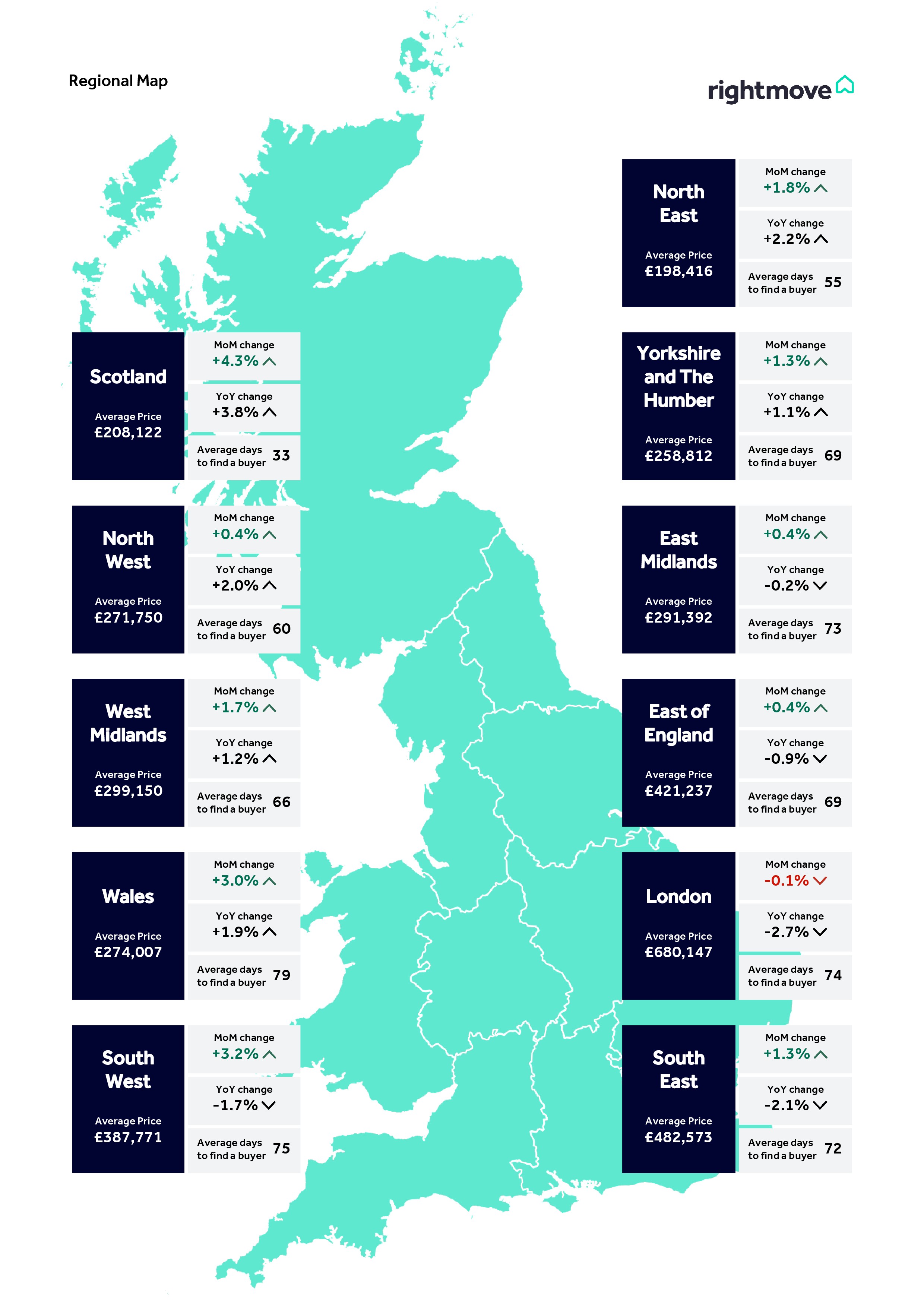

Babcock highlighted Scotland as an area demonstrating notable resilience, with average prices climbing by over 4%. This strength is attributed to a combination of lower average asking prices and a more streamlined home-buying process in the region.

“However, for most of the market, the combination of rising mortgage rates and the number of homes for sale being at its highest level for the time of year over a decade means that competitive pricing is crucial for sellers looking to attract buyer interest and secure a sale this spring,” Babcock added.

Mortgage Rates and Future Outlook

The trajectory of mortgage rates remains a key concern. Matt Smith, a mortgage expert, observed a shift in market sentiment. “At the start of the year, there was growing optimism that the Bank of England’s base rate would continue to fall, but that picture has shifted,” he stated.

While the initial shock of rate increases appears to have subsided, with rates stabilizing in recent weeks, they remain at elevated levels. The future direction of rates will hinge on upcoming inflation data and the Bank of England’s policy responses. Current market expectations point towards a period of relative stability rather than significant rate reductions.

Encouragingly, several lenders have recently reduced their mortgage rates, influenced by a decrease in swap rates, which are integral to how lenders price their offerings.

Buyer and Seller Psychology

Marc von Grundherr, director at Benham and Reeves, elaborated on the psychological impact of the current market conditions. “The combination of heightened geopolitical uncertainty and the increase in mortgage rates has understandably caused some buyers to pause for thought, particularly across the higher end of the market where affordability is already stretched,” he explained.

“However, what we’ve seen is not a collapse in confidence, but a more cautious and considered approach from both buyers and sellers,” von Grundherr continued. He also noted that London, often a lagging market, shows early signs of recovery, particularly in areas with realistic pricing and perceived long-term value.

Mark Wiggin, director at Mark Wiggin Estate Agents, emphasized the critical role of pricing. “Buyers start with three things: the price, the photos, and how long a home’s been listed,” he said. “If something’s been on the market for more than a few months, buyers immediately assume it’s overpriced. In this market, sellers must respond to that feedback – the market always tells you when the price isn’t right.”

Polly Ogden Duffy, managing director at John D Wood & Co, echoed this sentiment, particularly concerning the supply of flats. “With an increased supply of homes – particularly flats lingering from 2025 – buyers have more choice and are less inclined to engage with overpriced properties, meaning sellers who price too ambitiously risk missing out on serious, proceedable buyers.”

Conversely, the market for family homes continues to perform robustly, especially in areas with desirable school districts. Here, demand can still outpace supply, occasionally leading to multiple bids.

Peter Ryder, managing director at Thorntons Property Services, pointed to the East of Scotland and Inverness as areas demonstrating sustained resilience amidst broader economic uncertainties.

Rental Market Trends

In parallel with the sales market, separate research from Hamptons indicates an acceleration in rental price growth for newly-let homes in March. The average monthly rent for newly-let properties across Britain saw an increase, with annual growth doubling from 0.5% in February to 1.0% in March, reaching an average of $1,373 per month.

Aneisha Beveridge, head of research at Hamptons, commented, “While rents fell last year, early signs suggest the pace of rental growth is beginning to pick up as tenant demand rebounds.” The Hamptons lettings index, which uses data from the Connells Group, tracks achieved rents rather than advertised prices.

The data from Hamptons highlights regional variations in rental price growth:

- London: $2,305 (2.2% annual change)

- East of England: $1,260 (0.6% annual change)

- South East: $1,465 (0.0% annual change)

- South West: $1,247 (0.2% annual change)

- East Midlands: $999 (1.8% annual change)

- West Midlands: $1,087 (1.2% annual change)

- North East: $823 (-1.3% annual change)

- North West: $1,028 (0.9% annual change)

- Yorkshire and the Humber: $917 (0.2% annual change)

- Wales: $879 (-0.8% annual change)

- Scotland: $1,014 (0.8% annual change)